Could the current financial crisis have given us a reprieve from a boom in nuclear power spreading around the world? Not if my recent visit to URENCO is any indication!

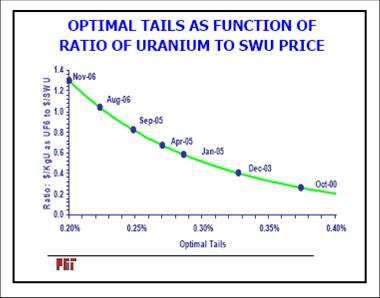

Many have argued that the so-called “nuclear renaissance,” will bring a dramatic increase in the use of nuclear power. Others point to the shaky financial legs new reactors stand on in the United States where it is estimated that a new reactor nuclear power plant costs about $13 billion; more than the net worth of the company building it! And this was before the current economic crisis. Now, with credit tightened to straightjacket levels, it seems nearly impossible to believe any new plants will be built in the US. Furthermore, as Tom Neff has pointed out, there is a relationship between enrichment capacity required and the price of natural uranium. As the cost of uranium goes up, enrichment facilities find it more cost effective to dig deeper, if you will, into the feed stock and extract more of the U235 in natural uranium. They are balancing the increased operating costs of extracting more from the “tails” or waste depleted uranium with saving money by buying less feed stock.

from Thomas Neff’s “Uranium and Enrichment: Supply, Demand, and Price Outlook”

Neff used this, before the crash of energy costs, to argue that suppliers of enrichment services would quickly find it economically advantageous to add to their enrichment capacity. At the time, most analysts were saying that there was a glut of enrichment services with about 55 million SWU-kg/year capacity while there was only a “need” for about 45 million SWU-kg/year. In that analysis, this “excess” capacity would quickly disappear as enrichment suppliers shifted to enrichment with lower tails and hence the need for greater separative work done. Now, of course, the prices of all commodities have fallen, including uranium, and it would appear that we should once again have a glut of enrichment, shouldn’t we?

However, URENCO and TENEX are still modernizing and expanding their capacities and, or so I understand, URENCO at least is not having any problems obtaining loans from banks. Of course, our banking industry is not the genius at predicting the future they once thought they were. Could they simply be slow in reacting to the current economic crisis?

Actually, there might very well be economic reasons why URENCO should be expanding its enrichment capacity in this time of low uranium prices. (I wouldn’t even try to guess about TENEX with its history of Soviet and Russian government investment.) These reasons draw heavily on URENCO’s status as an established supplier of enrichment services and further emphasize the difficulties nuclear-have-nots would face in trying to compete in the nuclear market. URENCO has an increasing number of centrifuges that have reached and even surpassed their amortized lifetime: they are basically profit cows. (Profit is very much a function of bookkeeping.) The same is true of nuclear power plants whose lives have been extended. URENCO could use its high profit, older cascades to finance its expansion program. Furthermore, the uranium it buys from its costumers now will be bought at rock bottom prices and will, presumably, not be fully exploited with the tails left with high levels of U235. Since the customers do not take back the tails, these could be saved for times of higher uranium prices. (URENCO has already sold tails to TENEX for further exploitation.)

I’m not totally convinced that it makes sense for URENCO to still be expanding its enrichment capacity. But the real issue here, as it is in all economics, is what the majority of consumers believe. If the world’s nations believe that fossil fuels are drying up—and they are—and that nuclear power is a way of producing cheap energy into the future, then the demand should increase, regardless of even major fluctuations in the price of oil. That could mean that the current economic crisis has only given us a brief respite from the mushrooming of nuclear fuel cycles. A concurrent crisis is the political disagreement over what that implies for nonproliferation. The nuclear-haves view this one way, and the nuclear have-nots definitely view it a different way. The later are more and more viewing the NPT as an exercise in preventing the spread of nuclear profits rather than nuclear weapons. Since I have listed the expansion of nuclear power as a crisis, I suppose you can see which side I come down on this. That doesn’t mean, however, that I believe the opposite view can be dismissed out of hand. We need to address both views as equitably and fairly as possible. One way of doing that would be to have multinational nuclear arrangements that really do share the profits.

But fundamentally, even nuclear energy is based upon limited natural resources

The “nuclear renaissance” is just a bunch of hype, about to crash on the rocks of reality.

Some people believe that the first wave of nuclear build some 30+ years ago ended because of the accident at Three Mile Island. Not so. It died (just as it is now) because of skyrocketing costs coupled with a bad credit environment. The surge in energy costs at the time – rather than creating a market for atomic plants, instead triggered a wave of energy efficiency, killing the demand for new supply.

I created this graph of US reactor orders. Notice that the market collapsed before the accident.

To create the nuclear generating capacity to power a single 100 watt light bulb costs on the order of $1000 dollars or so (and does not include credit costs, fuel costs, O&M, decomm, etc.)

To replace that 100 watt lamp with a 25 watt compact fluorescent lamp costs $3.

Adam Smith’s “Invisible Hand”, is about to again smack the atomic industry upside the head.

I’m sorry, but this post is so poorly written, I honestly haven’t the slightest idea what your point is. As best I can tell, the argument goes: – Nuclear is wildly expensive. – Therefore, no reasonable country/company will build new plants or need additional enrichment plants – Additional enrichment plants don’t make sense anyway when U is cheap. – But we all know the financial industry is filled with idiots who will probably finance nuclear power plants and enrichment plants anyway (ahh, if only everything were run by physicists – no, wait, they are responsible for the derivatives market). – Therefore we have a nonproliferation crisis that can only be avoided by following the approach advocated by the author in 2006.

Is that about it? Seems a bit thin for a post on this blog.

Leaving that aside – and assuming that the author is unable to rescue us all from our own stupidity and more nuclear power plants are built, wouldn’t it be in our interest to have existing suppliers expand their capacity so as to discourage new entrants? And, for the record, nuclear power plants are expensive, but they won’t cost $13B. Try 7-8.

Geoff,

I think you’re ignoring the broader story of what’s happening in the enrichment market. The biggest single source of uranium to the US market is the HEU-LEU deal and that expires in 2103. Under a pending follow on agreement Russian SWU will then drop from about half to a quarter or less of US supply. Meanwhile, the world’s remaining gaseous diffusion plants for EURODIF (in France) and USEC (in the US) are about to be shut down. New plants are about to start up in both places, but there’s probably a fair chance of delays in construction leaving a SWU gap and providing an opening for the existing TENEX and URENCO plants—one reason Russia has resisted a new HEU-LEU agreement.

Moreover, it should be recalled that both TENEX and URENCO are primarily government-owned, which may mean that they are not bound by some traditional business considerations

Also, for you or any of your readers who are interested in more on TENEX and the Russian nuclear industry, the Centre for International Governance Innovation has just published a paper I wrote on status and prospects of the Russian nuclear industry.